Entering 2023, the “dismal science” of economics certainly lived up to its name. Predictions of “rolling recessions” in developed economies were commonplace, a position we too held a year ago. Thankfully, we were wrong. Instead, global growth, estimated at circa 3% was only modestly below its long-term average.

A better-than-expected performance from the United States is key in this outturn. In the third quarter, the US grew at a heady 5% annualised pace, and looks set to grow by over 2% for the full year. Two cyclical factors and one structural element have been important here.

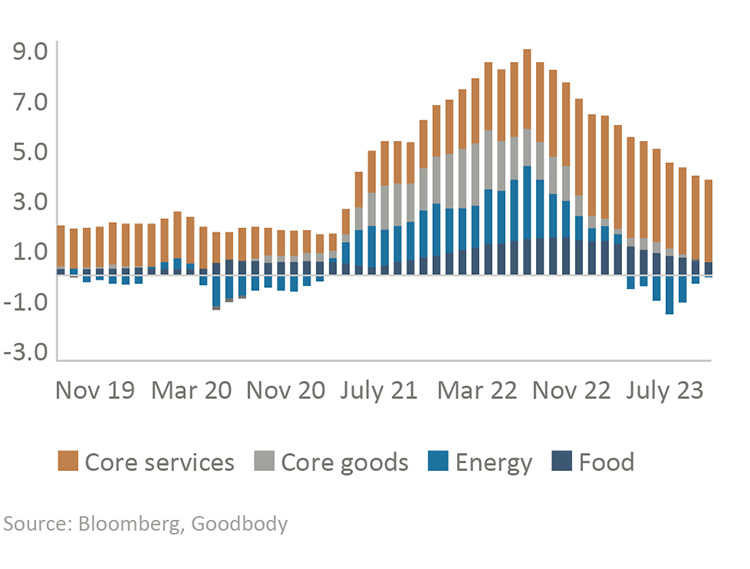

Most prominently, consumer spending, accounting for c.70% of US GDP, has continued to expand. A robust labour market has helped, but so has the rather unique feature of a drawdown of excess savings built up over the pandemic lockdowns. These savings peaked at over $2trn but have been consistently depleting. While estimates are uncertain, it is likely that these savings will soon be fully exhausted. With the household savings ratio at close to all-time lows at 3% and the Federal Reserve determined to reduce inflation through a softer labour market, a weaker outlook for the US consumer is in store for 2024.

The second cyclical factor helping growth has been a bigger government contribution. This has been surprising considering the strong economy. Much could change depending on the make-up of next year’s elections, but it is

likely that fiscal policy will not be stimulatory in 2024. Throw in the lagged impact of tighter monetary policy and the ingredients are there for a US recession over the coming quarters, albeit a mild one.

Figure 1. US interest rate cutting cycles since 1955

| Year | Median (%) | Current level (%) |

| Rate peak/Current rate | 6.1 | 5.3 |

| Rate trough | 3.5 | TBC |

| Cumulative rate cuts | -2.9 | TBC |

| Core inflation rate | 3.6 | 4.0 |

| Unemployment rate | 5.9 | 3.9 |

| Growth rate | -0.2 | 1.2 |

Source: Federal Reserve, FactSet, Goodbody

Economic weakness in Europe

Outside of the US, there is already evidence of economic weakness in Europe. The manufacturing sector has been in contraction for all of 2023, while the services sector has recently joined it.

Germany, the euro area’s largest economy, is in the biggest bind due to its energy vulnerabilities and threats to its auto industry from the shift away from fossil fuels and competition from China. The French economy has already begun to contract recently, suggesting that the euro area may already be in recession. The UK economy is flatlining at best.

Opportunities and risks from structural factors

With central bankers keen to keep the foot on the monetary brakes until they have clear evidence that the inflation risk has passed, and governments under market pressure to get their fiscal house back in order, there are few cyclical growth drivers on the horizon in the short-term.

There are, however, important structural factors that bring both opportunities and risks for the economic outlook. Firstly, the energy transition is now in full flow, with all the global superpowers aiming to put their own mark on it.

Secondly, the AI revolution took a giant leap forward this year. While the benefits, risks and direction of this revolution are unknown, it is clear it is not going away. Managed properly, it has the potential to reap huge productivity benefits. Due to the global import of these issues, a race has begun to finance and build the required infrastructure to enable these trends to take place.

These issues go beyond economics and will have huge geopolitical implications. With about 50% of the world’s population due to go to the polls in various elections in 2024, there is a lot at stake.

This article was originally published in the Goodbody Investment Outlook 2024: Going for (structural) growth publication on 4 December 2023. To read the full Investment Outlook publication, click here.

This is a marketing communication.