What’s going on in financial markets? Which macro themes should you watch? Drawing on our depth and breadth of market and economic expertise, Market Pulse brings you insights on the latest investment themes to help preserve and grow your wealth.

Market views

- It was another risk-off week for equities. For a change, it wasn’t rising bond yields causing the falls. Geopolitics seemed the main concern despite limited impact on energy prices. Global equities declined 1.8% in euro terms (also -1.8% in local currency). Europe ex-UK was the best performing region, and the US was the weakest. Overall, sector performance was led by defensives (ex Health Care) but Materials and Consumer Discretionary were amongst the leaders. Energy was a laggard as the oil price settled lower. Bond yields fell slightly last week in the US and Europe, despite stronger than anticipated US economic data. This week has started with a broad rally reflecting earnings, less geopolitical fear, and lower US Treasury Q4 borrowing estimates.

- Half of the S&P 500 has reported Q3 results and there is an improving trend compared to last week. Reported growth improved to 6.5% year-on-year (y/y) from 4% last week, while the earnings ‘beat’ vs consensus increased to 8% (from 7%) compared to a ‘normal’ 5%. The skew of share price reactions still seems negative based on understandably cautious outlooks. Europe’s more limited reporting by 40% of the STOXX Europe 600 has been slightly behind expectations with -9% y/y growth. It’s too early to gauge overall 2024 earnings revisions.

- There’s been a lot of new information for markets to digest recently between macro-economics, geopolitics and earnings. The key pending data points are the US employment report (which will be released on 3 November), the US ISM Manufacturing Index (1 November) and the US Federal Reserve FOMC announcement (1 November), where no change in rates is expected.

Macro views

- The European Central Bank (ECB) announced no policy changes at its meeting last Thursday. Policy rates were held stable, as were asset purchase programs and bank reserve requirements. The ECB statement reiterated that it thinks policy rates are at levels that, if sustained, will contribute to lower inflation.

- The initial estimate of US Q3 real GDP growth surged to 4.9% in Q3 (seasonally adjusted annualised quarter-over-quarter growth) compared to consensus forecasts of 3.8%. The growth was driven by strength in consumer and government spending, offset by a slowdown in business investment. Inventory investment boosted growth by 1.3% which will likely supress future growth as it unwinds. Within the data, Core PCE inflation continued to slow to 2.4% in Q3.

- Purchasing manager indices (PMIs) released last week show a continued slowing in Europe where both services and manufacturing were down compared to last month and weaker than anticipated. The US surveys saw slight upticks versus last month and came in slightly better than anticipated, although growth has clearly slowed from earlier in the year.

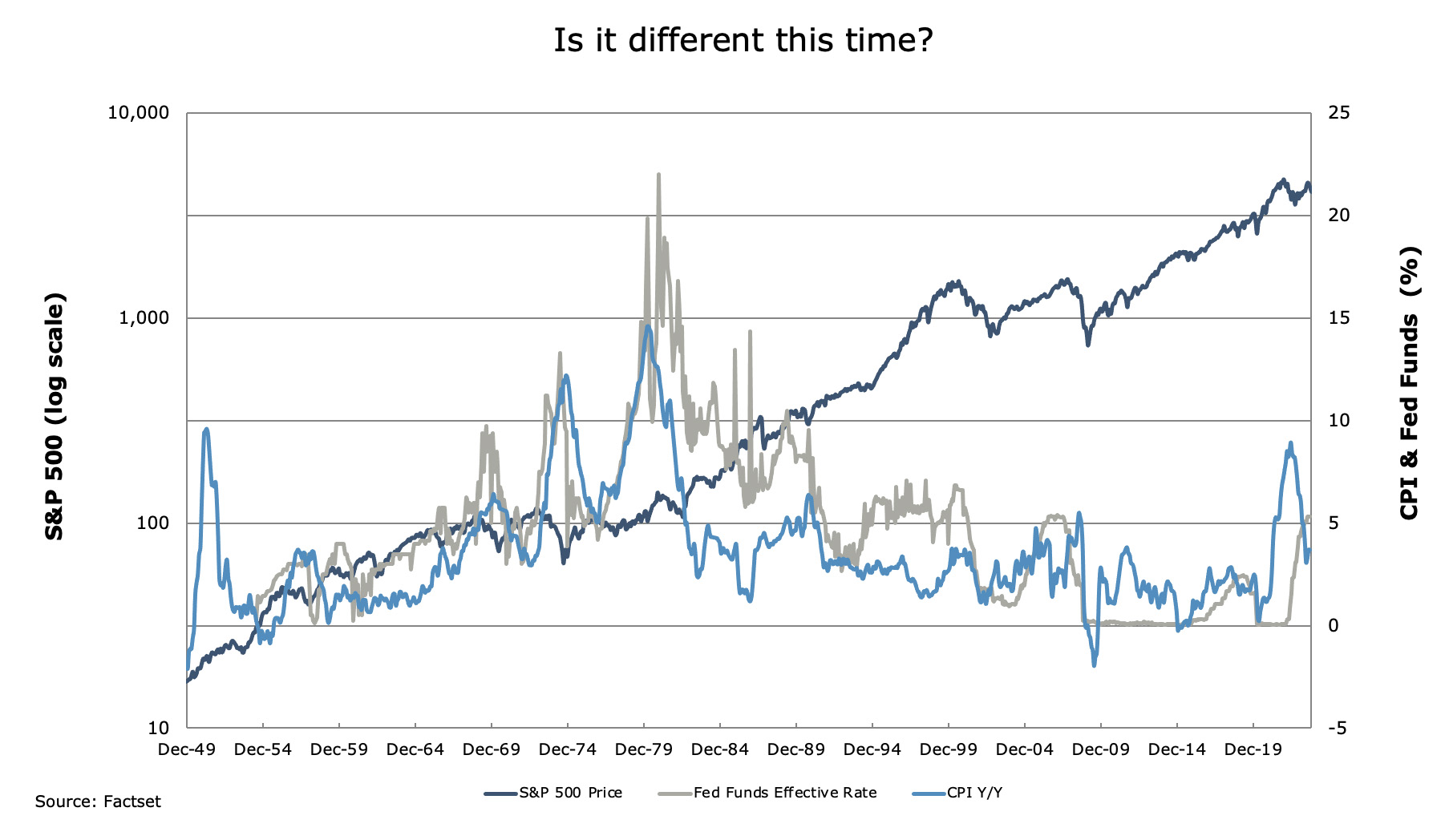

Chart of the week

Our chart shows a long-term history of the S&P 500, US inflation (consumer price inflation, CPI) and policy rates. Since 1950, there have been seven periods when US CPI peaked over 5% y/y. The current episode is unique in that it is the only one where the Fed policy rate was still rising 12 months after the peak in CPI. This may reflect the central bank’s delayed reaction to the post-pandemic inflation. The prior episodes almost all had recessions, with spikes in energy prices being a driving factor. The global financial crisis episode is the only one where the S&P 500 wasn’t higher 12 months after the CPI peak, and the 1980 episode (double dip recession) is the only one where the S&P declined from 12 to 18 months after the CPI peak. Unfortunately, this doesn’t tell us how the future will unfold.

What would you like to do next?

Talk to us | Read more insights | Read our investment approach |